PARTICIPATING IN A MARKET ECONOMY

In a market economy, buyers and sellers use the marketplace to make economic decisions. Buying decisions are made by consumers—including individuals, businesses, and government. A consumer is a person who buys and uses goods and services. The individual buying decisions of consumers have a tremendous influence on a market economy. Consumers decide what to buy, where to buy, from whom to buy, and what price they are willing to pay.

Successful producers must pay close attention to the needs and experiences of consumers. Producers are individuals and organizations that determine what products and services will be available for sale. Producers invest resources and take risks in order to make a profit. They determine what products and services will be available in the economy, what needs and wants they will try to satisfy, and the prices they want to receive.

It may seem that the economy is a big, unorganized system in which everyone pursues his or her own self-interest. You may wonder how the system can work when each business makes its own decisions about what to produce and charge, while each consumer makes a decision about what and where to buy and how much to pay. The system does work and works well based on the economic principles of supply and demand.

Consumers Set Demand

When consumers make decisions about what they will purchase, they determine the demand for goods and services. Demand is the quantity of a good or service that consumers are willing and able to buy. A business depends on demand for their products and services in order to make a profit. For example, if a new restaurant opens in your town, but the service is slow, the quality of the food is poor, and the noise level is high, will consumers continue to eat there? It is not likely. Suppose a new restaurant opens with terrific food as well as fast and friendly service. It will soon be packed with people who prefer that restaurant.

Producers Establish Supply

Understanding consumer demand helps businesses to determine what types and quantities of products to supply. Supply is the quantity of a good or service that businesses are willing and able to provide. If consumers want a popular product and are willing to pay a price that allows a business to make a profit, businesses will be willing to provide the product to meet the demand. On the other hand, if there is a greater supply of a product than consumers want or if customers are tiring of an older or poor quality product, businesses are less likely to continue to offer the product for sale.

In a market economy, buyers and sellers use the marketplace to make economic decisions. Buying decisions are made by consumers—including individuals, businesses, and government. A consumer is a person who buys and uses goods and services. The individual buying decisions of consumers have a tremendous influence on a market economy. Consumers decide what to buy, where to buy, from whom to buy, and what price they are willing to pay.

Successful producers must pay close attention to the needs and experiences of consumers. Producers are individuals and organizations that determine what products and services will be available for sale. Producers invest resources and take risks in order to make a profit. They determine what products and services will be available in the economy, what needs and wants they will try to satisfy, and the prices they want to receive.

It may seem that the economy is a big, unorganized system in which everyone pursues his or her own self-interest. You may wonder how the system can work when each business makes its own decisions about what to produce and charge, while each consumer makes a decision about what and where to buy and how much to pay. The system does work and works well based on the economic principles of supply and demand.

Consumers Set Demand

When consumers make decisions about what they will purchase, they determine the demand for goods and services. Demand is the quantity of a good or service that consumers are willing and able to buy. A business depends on demand for their products and services in order to make a profit. For example, if a new restaurant opens in your town, but the service is slow, the quality of the food is poor, and the noise level is high, will consumers continue to eat there? It is not likely. Suppose a new restaurant opens with terrific food as well as fast and friendly service. It will soon be packed with people who prefer that restaurant.

Producers Establish Supply

Understanding consumer demand helps businesses to determine what types and quantities of products to supply. Supply is the quantity of a good or service that businesses are willing and able to provide. If consumers want a popular product and are willing to pay a price that allows a business to make a profit, businesses will be willing to provide the product to meet the demand. On the other hand, if there is a greater supply of a product than consumers want or if customers are tiring of an older or poor quality product, businesses are less likely to continue to offer the product for sale.

A Graphic View

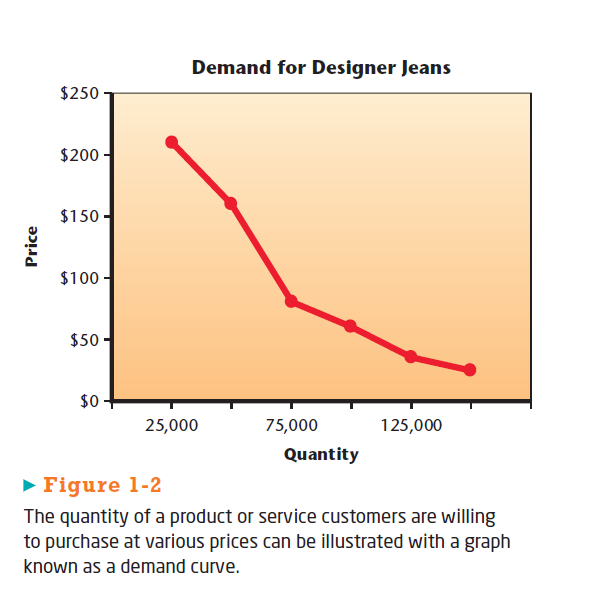

Demand and supply for a product or service can be illustrated using graphs known as demand curves and supply curves. The demand curve illustrates the relationship between the price of a product or service and the quantity demanded by consumers. As the price decreases, the number of consumers willing and able to purchase the product and the quantity they will purchase increases. Figure 1-2 illustrates the possible customer demand for designer jeans at various prices in a specific market.

Demand and supply for a product or service can be illustrated using graphs known as demand curves and supply curves. The demand curve illustrates the relationship between the price of a product or service and the quantity demanded by consumers. As the price decreases, the number of consumers willing and able to purchase the product and the quantity they will purchase increases. Figure 1-2 illustrates the possible customer demand for designer jeans at various prices in a specific market.

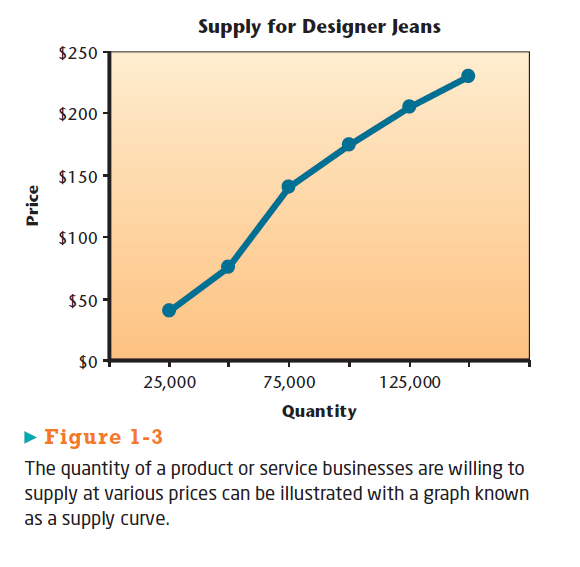

In the same way, the supply curve illustrates the relationship between the price of a product and the quantity businesses are willing to supply. At higher prices businesses will be willing to supply larger quantities of the product or service. Figure 1-3 illustrates the possible supply of designer jeans manufacturers are willing to provide to a market at various prices.

DETERMINING PRICE

Why is the price of a hotel room in Phoenix, Arizona, higher in winter than summer? Why do the prices of many of the products sold by farmers remain quite low? Prices are affected by the relationship between supply and demand, plus other factors.

Factors Influencing Demand

If many consumers want (or demand) a particular good or service, its price will tend to go up. More people vacation in Phoenix in the winter than in the summer so demand and prices for hotel rooms rise. When fewer people visit that area during the hot summer, the supply of hotel rooms is greater than the demand. Therefore, prices will decline.

When customers see a number of products that they believe will satisfy a particular want or need, demand for any one of those products will not be as high. Customers will be willing to switch from one product to another if the price of one is much higher than the others. When customers cannot find a good substitute for a product they want, demand for that product will be high. Even if the price increases, they will be willing to pay the higher price because they are unwilling or unable to switch to another choice.

Factors Influencing Supply

The supply of a product can also affect the price. Because the supply of many of the crops and livestock raised on farms is large, prices remain low. If a drought cuts the quantity of corn grown by Midwest farmers one year, the price of corn will increase.

Competitors are businesses offering very similar products to the same customers. As the number of competitors increases, so does supply. A business will not be able to easily raise its prices. It will have to be much more sensitive to the prices charged by its competitors.

When competition is limited, consumers cannot find good alternatives. If you live in a part of town where there is only one supermarket, the prices at that store will often be higher due to a lack of competition. The prices of products featuring new technology will often be high because the company offering the new product seldom has direct competition.

Sometimes a natural disaster or other unforeseen circumstance affects supply. If the supply of oil, gasoline, or water is disrupted, their prices will increase. The supply of other products that use those resources in production may also be affected and their prices can increase as well. Sometimes businesses will try to restrict supply of products in order to obtain a higher price. That will only work if customer demand is high and if there are no good substitutes for the product.

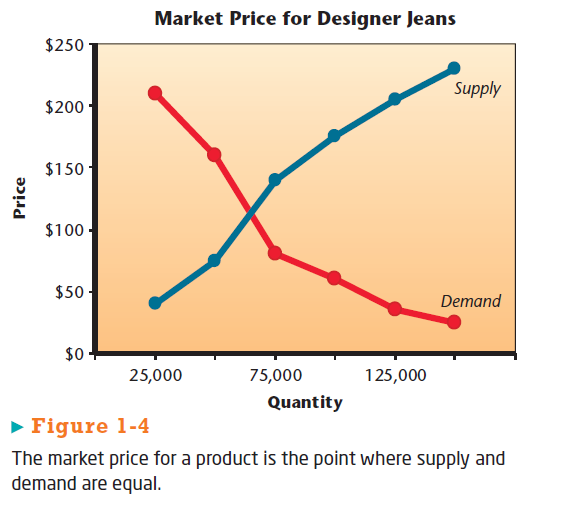

Determining Market PriceSupply, demand, and competition determine the market price for a product or service. The market price is the point where supply and demand are equal. Figure 1-4 shows the market price for designer jeans. Look at the point where the demand curve and the supply curve intersect. This illustrates that consumers are willing to purchase nearly 65,000 pairs of jeans and businesses are willing to supply that same quantity if the retail price is about $110 per pair.

Why is the price of a hotel room in Phoenix, Arizona, higher in winter than summer? Why do the prices of many of the products sold by farmers remain quite low? Prices are affected by the relationship between supply and demand, plus other factors.

Factors Influencing Demand

If many consumers want (or demand) a particular good or service, its price will tend to go up. More people vacation in Phoenix in the winter than in the summer so demand and prices for hotel rooms rise. When fewer people visit that area during the hot summer, the supply of hotel rooms is greater than the demand. Therefore, prices will decline.

When customers see a number of products that they believe will satisfy a particular want or need, demand for any one of those products will not be as high. Customers will be willing to switch from one product to another if the price of one is much higher than the others. When customers cannot find a good substitute for a product they want, demand for that product will be high. Even if the price increases, they will be willing to pay the higher price because they are unwilling or unable to switch to another choice.

Factors Influencing Supply

The supply of a product can also affect the price. Because the supply of many of the crops and livestock raised on farms is large, prices remain low. If a drought cuts the quantity of corn grown by Midwest farmers one year, the price of corn will increase.

Competitors are businesses offering very similar products to the same customers. As the number of competitors increases, so does supply. A business will not be able to easily raise its prices. It will have to be much more sensitive to the prices charged by its competitors.

When competition is limited, consumers cannot find good alternatives. If you live in a part of town where there is only one supermarket, the prices at that store will often be higher due to a lack of competition. The prices of products featuring new technology will often be high because the company offering the new product seldom has direct competition.

Sometimes a natural disaster or other unforeseen circumstance affects supply. If the supply of oil, gasoline, or water is disrupted, their prices will increase. The supply of other products that use those resources in production may also be affected and their prices can increase as well. Sometimes businesses will try to restrict supply of products in order to obtain a higher price. That will only work if customer demand is high and if there are no good substitutes for the product.

Determining Market PriceSupply, demand, and competition determine the market price for a product or service. The market price is the point where supply and demand are equal. Figure 1-4 shows the market price for designer jeans. Look at the point where the demand curve and the supply curve intersect. This illustrates that consumers are willing to purchase nearly 65,000 pairs of jeans and businesses are willing to supply that same quantity if the retail price is about $110 per pair.